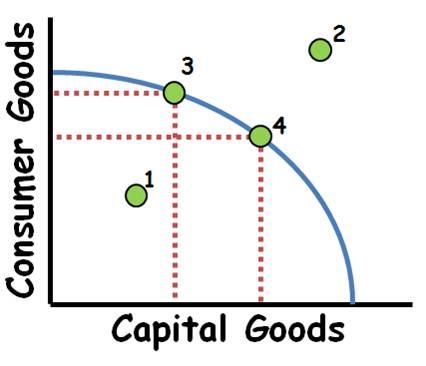

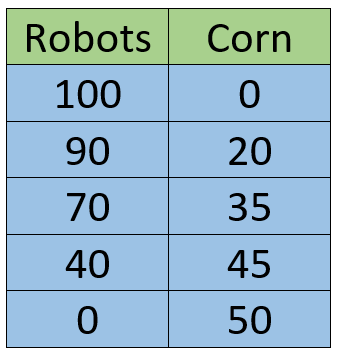

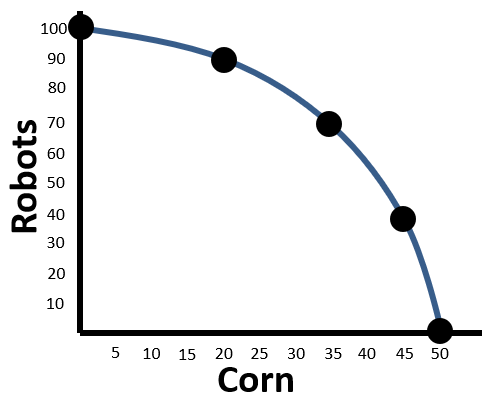

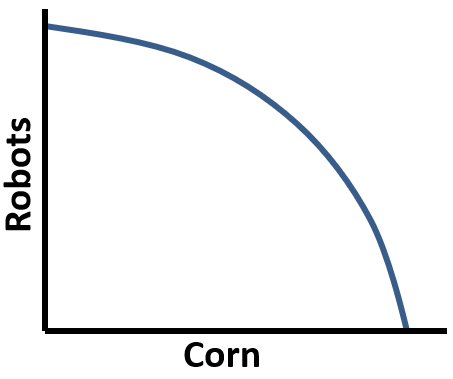

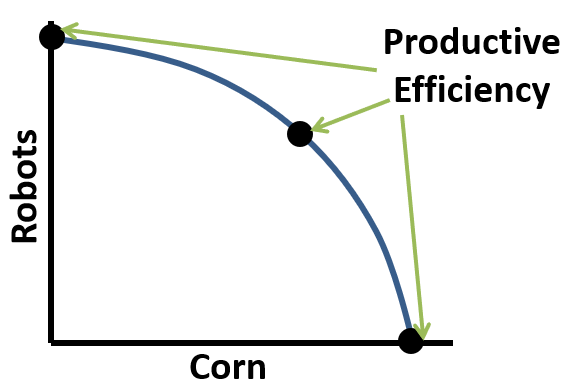

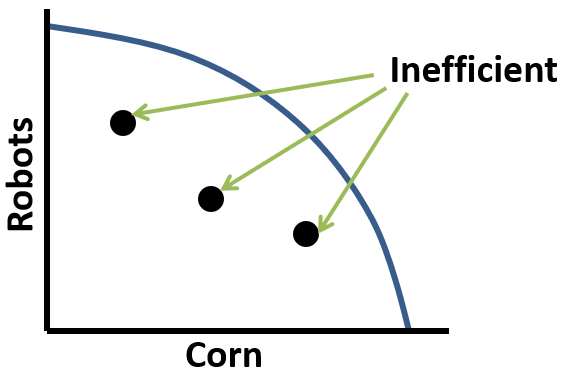

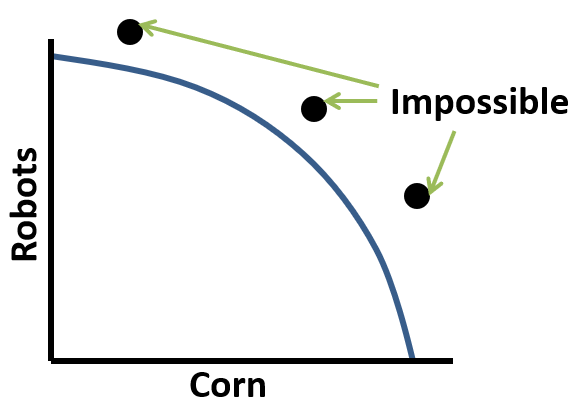

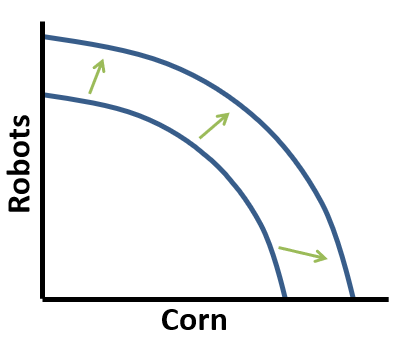

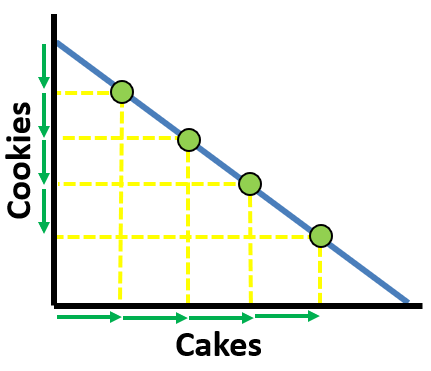

Here are some key concepts and an activity I just finished to help you practice working with the Production Possibilities Curve. This one applies to both Micro and Macro economics. This graph always shows up on both exams. There are 20 different scenarios to test your knowledge. Give it a try and see if you have what it takes to answer all 20 correctly!